Phosphorus:

Output: Weekly output reaches 20,5kt, up 5.97% WoW, with capacity utilization at 68.4%. The operation rate is generally above 65% in Yunnan, Guizhou, and Sichuan.

Price: Average price slightly rose to CNY22,895/t but later down to CNY22,830/t. The 2 week’s high level made buyer side hesitate as the downstream production cost needs control.

Outlook: Low hydro-power costs bolster the production, but weak demand and buyer resistance may extend the bearish trend. Prices could slide further.

Phosphoric acid:

Average price of 85% H.P. phosphoric acid rose 0.75% WoW to CNY6,730/t, with regional variations (e.g. Yunnan stable at CNY6,600/t). The increase was driven by high yellow phosphorus cost (avg. CNY22,829/t). Wet-process P.A. price averaged at CNY6,850/t, about 1.15% lower MoM.

Sulfur:

Price: Spot prices fell 0.69% WoW to CNY2,324/t (Shandong port), Zhenjiang port price drops from CNY2,385 to CNY2,324/t. High port inventory (2.41 mln tons) and downstream resistance drove the price decline.

Output: Domestic output remained stable, while June imports surged 23.75% YoY to 988.4kt.

Urea:

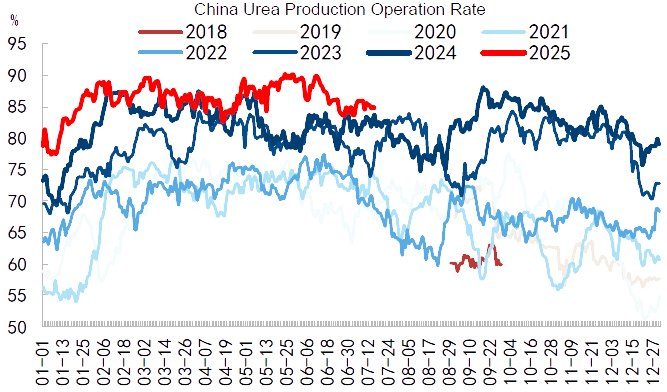

prices fluctuated narrowly, urea prilled is offered at CNY1,770-1,840/t in Shangdong. Urea futures surged 2.73% to CNY1,806/t, driven by export demand and general positive sentiment. Supply is sufficient as daily output is about 195.5kt with an operation rate of 83.5%. In-factory inventory is 895.5kt(-72.2kt) and port inventory is 541kt(+52kt). Compound fertilizer production operation rate is up to 32.55% (+2.72%). Amsul average price fell 2.97% WoW to CNY1,196/t. Coking grade operating rate drops to 73.96% (-1.4% WoW), but caprolactam grade output is stable, it maintained an ample supply and sale still has pressure.

Potash:

Price: Imported MOP: 62% white crystal port prices surged to CNY3,650/t (+200/t), but turns down due to policy intervention, with some traders offering CNY3,300/t. Domestic sources follow up with the trend (e.g., Qinghai Salt Lake up-regulates offers to CNY2,900/t EXW).

SOP: Mannheim 52% powder rose 1.35% WoW to CNY3,770/t.

Output & Supply: Port inventory is stable at 1.99mln tons level, the domestic MOP output is down to 2.53mln tons in H1 (-17.1% YoY). Operation rate generally declined: MOP 49.84%, SOP (Mannheim 53.29%)

MAP/DAP:

MAP production tends to tight as producers need to hurry for autumn fertilizer reserves.

SCFI is 1,647(-86), keeps down in the last 6 weeks CCFI is 1,303 (-0.8%). Freight to EU/Med lines is stable.