Phosphorus: as the market doesn’t accept too high cost, P4 price slides. Benchmark price comes to CNY28,562/t. Yellow phosphorus operation rate is 48-52%, with some facilities maintenance in Yun’nan and some resumes in Sichuan. P4 weekly out put is around 14.6kt. Supply is constrained by energy consumption controls (still in dry season), environment protection inspections, and capacity replacement policy. Downstream demand for glyphosate and iron phosphate is robust, boosted by spring farming demand and overseas restocking, tightening supply–demand balance. On policy side, the govn’ strictly curbed new capacity and phased out outdated capacity.

Sulfur: sulfur market rebounds in a V-shape this week. Spot price of granular sulfur at Zhenjiang Port is CNY6,310/t (+2.6% WoW). International CFR prices soared to USD1,100-1,200/t, hits a historical high level. Shipment from middle east is still halted, while Turkey starts sulfur export ban. Market is in shortage supply but demand is surging, especially from Indonesia. China domestic refineries operation rate is 55%–60% and weekly output is about 8.5kt. The total social inventory is 299kt (-5% WoW). The market sticks bullish sentiment and traders are reluctant to sell. The sulfur tight supply situation is not easy to ease and fertilizers production cost won’t come down in a short time.

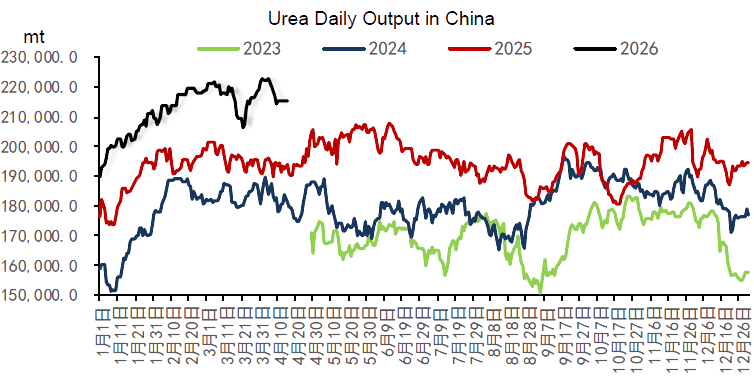

Urea: spot price is slightly lower this week. EXW price is CNY1,800-1,860/t. Operation rate is 89.95%, with weekly output of 1.5mln tons. In-factory inventory is 464kt(-43.4kt), port inventory is 147kt(-5kt). The general inventory remains at a low level and keeps destocking. The current market sentiment is cautious, as producers hold firm offering, while traders and downstream buyers purchase on rigid demand.

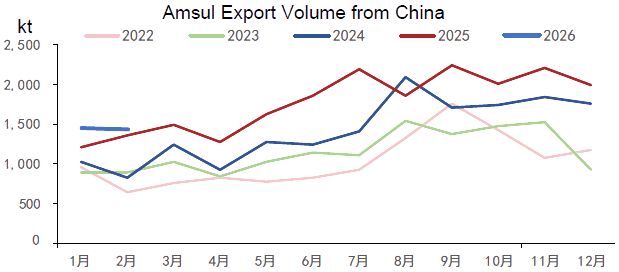

Amsul market stays high in late April. The coking grade price is CNY1,480-1,500/t, caprolactam grade is CNY1,780-1,820/t. Production operation rate is still around 70-75%, relatively steady.

Policy: urea export with quota would start since May. Phosphorus fertilizers export is still unclear, but factories still have export quota for urea. However, market predicts that the urea export price won’t be low as the CIQ would still have price regulations for export cargo.

SCFI is 1,875 (-11), CCFI is 1,234(+1.9%).