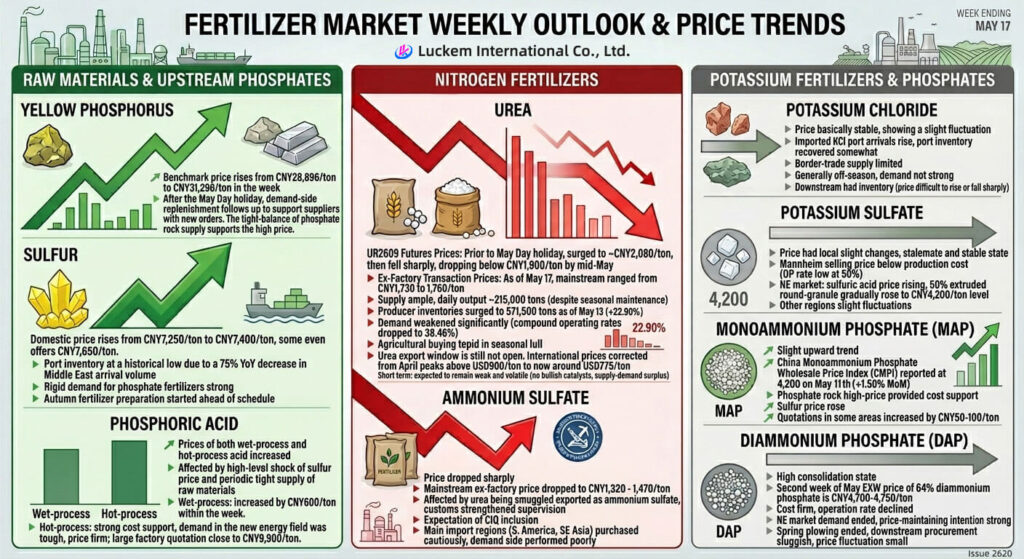

· Yellow phosphorus: The price showed an upward – trend. The benchmark price of yellow phosphorus rises from CNY28,896/t to CNY31,296/t in the week. After the May Day holiday, the demand-side replenishment follows up to support suppliers with new orders. The tight – balance of phosphate rock supply supports the high price of yellow phosphorus.

· Sulfur: The price continues to rise rapidly. The benchmark price of domestic sulfur rises from CNY7,250/t to CNY7,400/t, some even offers CNY7,650/t. The port inventory was at a historical low due to a 75% year – on – year decrease in the arrival volume from the Middle East. The rigid demand for phosphate fertilizers is strong, and the autumn fertilizer preparation started ahead of schedule, supporting the sulfur price.

· Phosphoric acid: The prices of both wet-process phosphoric acid and hot-process phosphoric acid increased. Affected by the high – level shock of sulfur price and the periodic tight supply of raw materials, the wet-process phosphoric acid increased by CNY600/t within the week. Due to the high price of yellow phosphorus, the hot-process phosphoric acid had a strong cost support, and the demand in the new energy field was tough, so the price was firm, and the quotation from large-scale factories was close to CNY9,900/t.

· Urea: During the past two weeks, the urea market shifted from a peak to a sustained downward trend. Prior to the May Day holiday, futures prices for UR2609 surged to around CNY2,080/t, but then fell sharply, dropping below CNY1,900/t by mid-May. As of May 17, mainstream ex-factory transaction prices ranged from CNY1,730 to 1,760/t. Supply remained ample, with daily output hovering around 215,000 tons despite seasonal maintenance shutdowns. Demand weakened significantly as compound fertilizer operating rates dropped to 38.46%, and agricultural buying remained tepid in the seasonal lull. Consequently, producer inventories surged to 571,500 tons as of May 13, a 22.90% increase from the previous period. Urea export window is still not open. International urea prices corrected from their April peaks above USD900/t to now around USD775/ton. In the short term, with no significant bullish catalysts and a clear supply-demand surplus, the market is expected to remain weak and volatile.

· Ammonium sulfate: The price dropped sharply, and the mainstream ex – factory price dropped to CNY1,320-1,470/t. Affected by the incident of urea being smuggled exported as ammonium sulfate, the customs in many places strengthened supervision. The market had an enhanced expectation that ammonium sulfate would be included in the CIQ required list. At the same time, the main import regions such as South America and Southeast Asia purchased cautiously, and the demand side performed poorly.

· Potassium chloride: The price was basically stable, showing a slight fluctuation. Imported KCl port arrivals rise, and the port inventory recovered somewhat. However, the border – trade supply was limited. It was generally in the off – season, and the demand was not strong. The downstream had inventory, so the price was difficult to rise or fall sharply.

· Potassium sulfate: The price had local slight changes, and was generally in a stalemate and stable state. The selling price of Mannheim potassium sulfate is below it’s production cost, and the operating rate remained at a low level of 50%. In the Northeast market, due to the rising price of sulfuric acid, the quotation of 50% extruded round – granule potassium sulfate gradually rose to CNY4,200/ton level, and the prices in other regions had slight fluctuations but little change.

· MAP: The price showed a slight upward trend. The China MAP Price Index (CMPI) reported at 4,200 on May 11th (+1.50% MoM). The high – price operation of phosphate rock provided cost support, and the sulfur price rose, so the enterprises maintained high prices, and the quotations in some areas increased by CNY50-100/t.

· DAP: It was in a high consolidation state. In the second week of May, the EXW price of 64% DAP is CNY4,700-4,750/t. The cost was firm, the operation rate declined, and the demand in the Northeast ended, so the enterprise’s price – maintaining intention was strong. However, the spring plowing ended, and the downstream procurement was sluggish, so the price fluctuation was small.