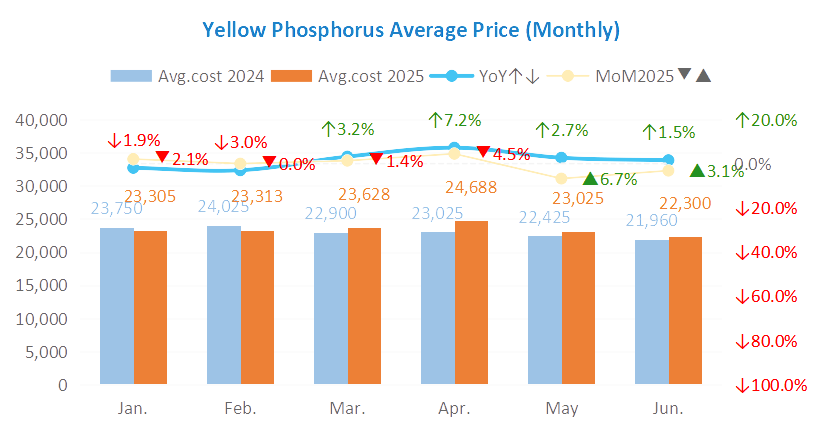

Phosphorus: price edged up, the benchmark price rises to CNY22,346/t on Jul 4th, +0.70% MoM. Most deals are closed at about CNY22,200/t in Yunnan/Sichuan, CNY22,350-22,400/t in Guizhou. The supply-side holds firm, but market demand is weakened. P4 supply rises 5.98% (20.72kt) as hydropower boosted output, the demand side resists high offers. Market price may dip to CNY22,100-22,300/t this week, about CNY50-100/t lower. The avg. cost in June is 0.8%-1.0% higher from May, MoM. Driven by ample supply (hydropower season) and weak demand, P4 avg. price is CNY22.3-22.5k/t in H1, 2025, about 4%-5% lower vs 2024H1 (midpoint CNY23.5k/t).

Phosphoric acid: the average price of 85% industrial-grade phosphoric acid in China is CNY6,640/t, down 0.75% WoW. The rising yellow phosphorus cost can’t help to lift demand, as the market remains sluggish. P.A. prices are expected to hold steady with narrow fluctuations.

Sulfur: Yangtze River port granular sulfur cost slid from CNY2,320 to CNY2,280/t (-1.72%), while liquid/solid sulfur in south and southwest China dropped CNY20-50/t. It is resulted by lower tender pricing and sluggish demand. Inventory: port inventory dipped to 2.32mln tons (-0.5% WoW), about 10.32% lower YoY.

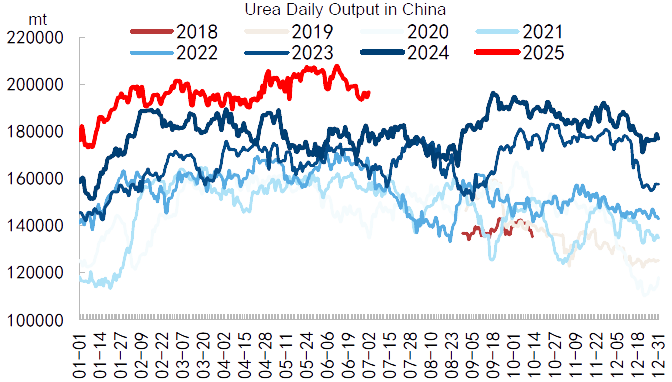

Urea: prices fluctuated narrowly, urea prilled is offered at CNY1,760-1,790/t in Shangdong. Supply is sufficient as daily output is about 197kt with an operation rate of 84%. In-factory inventory is 1,018.5kt(-77.4kt) and port inventory is 440kt(+59kt). The agricultural top-dressing fertilizers demand (for corn in north/central China) provides support, but compound fertilizer demand is weakened(operation rate is down to 29%). Amsul price declines broadly. In Shandong, the coke-grade price falls 2.6% to CNY1,125/t, while caprolactam-grade drops 2.94% to CNY1,155/t. The coke-grade operating rate dipped to 73%, while caprolactam-grade surged to 95.8%. Demand remains sluggish, as compound fertilizer operating rates expected to decline.

Potash: Port 62% MOP hit CNY3,400–3,450/t, potash from Qinghai Salt Lake offers CNY2,700/t (+100), the uptrend is driven by low port inventories (1.98mln tons, about 29.8% lower YoY) and traders’ hoarding. Supply tightness will support potash offering in short term. Pushed by a higher production cost, 52% powder cost is CNY3,900-4,000/t(+150-200/t), but weak seasonal demand limits high-price acceptance. MKP and NOP cost is also following the uptrend.

MAP/DAP: MAP price is stabilized amid tepid demand. 55% powder grade is CNY3,400-3,550/t. Downstream compound fertilizer factories maintained cautious procurement due to slow autumn fertilizer pre-sales.

SCFI is 1,763(-98), CCFI is 1,343 (-1.9%). Global container indices are in downtrend.