Phosphorus: the yellow phosphorus price fell to CNY22,200-22,400/t (EXW cost with payment term of acceptance bill) in Yunnan/Guizhou/Sichuan, about 1.3% lower in the week. Weak demand and rising supply (weekly output is 19kt, +0.4%) drove the decline. Prices may further dip amid weak negotiations. High supply and cautious downstream purchasing intensify downward pressure. Key factors: Southwest China’s rainy season lowered hydroelectric costs, reducing production expenses. The downstream sectors like phosphates maintained low procurement.

Phosphoric acid: the P.A. market saw mixed trends. Wet-process P.A. price dipped slightly.

Sulfur: the market diverged: Zhenjiang port solid sulfur rose 9.8% to CNY2,485/t due to the tension in Middle East, while Shandong liquid sulfur fell to CNY2,220/t as demand is weak. Port stocks slid slightly, with phosphate fertilizer demand providing support.

SCFI is 1869 (-218), CCFI is 1342 (+8%). Freight from far east to US diverged sharply, plunged to USD2,772/ctn to US west coast.

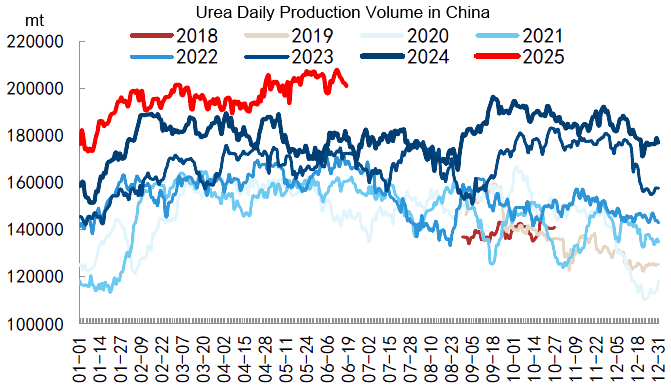

Urea: the dealt price is CNY1,790-1,840/t (+90/t) in Shangdong. The weekly volume is 1,430.7kt(+17.5kt), operation rate 88.28%. In-factory typical inventory is 1,136kt(-41.1kt). The port typical inventory is 295kt(+50kt). The operation rate is 31.82%(-1.99%) for compound fertilizers and 64.32%(+0.55%) for melamine. Urea FOB costs USD355/t(-5/t). Amsul price keeps strong at above CNY1,080/t(+24/t). Caprolactam plant cutbacks (operating rate down to 5.7%) reduced the output. While Latin American procurement peak pushed spot FOB price to above USD155/t. Impacted by the global urea price and Middle East tension, the market will remain bullish in short term.

Potash: After the new contract price USD346/t settled, KCl port price is supported (62% white KCl at CNY3,100-3,250/t), but border trade price fell to CNY2,850-2,870/t. SOP 52% powder dropped to CNY3,550-3,700/t amid “off-peak season” atmosphere.

MAP/DAP: MAP price firmed up, rising CNY20-50/t due to the surging sulfur cost and increased export inquiries. 55% powder is CNY3,250-3,370/t. Domestic demand remains sluggish (post-summer fertilizer season, low compound fertilizer operating rates, high inventories), limiting purchases to rigid needs. Prices may consolidate in short-term, with potential increases from late July if autumn demand surges.

USD:CNY is stable at 7.15-7.17. Fed still has no plan to cut interest.