Phosphorus: the market continued its uptrend, with the benchmark price reaching CNY31,162/t (+4.1% WoW) in the southwest. As the U.S. lists phosphorus as a critical national defense material, it caused a renew assessment on global supply chain. In addition, the intl’ market has a strong demand for glyphosate restocking, while the domestic spring farming preparation for pesticides and the new energy industry demand both rise. Supply is tight as some factories has facilities maintenance plan in Yunnan. Traders hold the inventory with reluctance to sell, and export prosperity remains high.

Sulfur: the market is still running on the higher stage, though some offers come down, but the Changjiang River port granular sulfur price is still above CNY6,000/t. The port inventory keeps going down to a multi-year low level and widening supply-demand gap. Intl’ market, the FOB price in Middle East hits USD720-740/t, also a historical high level. The geopolitical tensions in the Middle East cut off Iranian supplies. As the sulfur import dependence is above 65%, tight supply would last the high sulfur price in China. China’s own sulfur output was 11.8 mln tons in 2025, import volume was lowered to 9.61mln tons but the average import price was higher to USD265.3/t. As the port inventory was lower to below 1.5mln tons for a long time, tight supply won’t be eased in the short term.

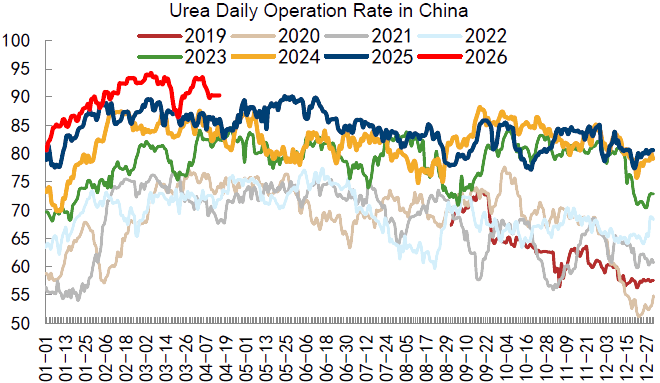

Urea: market is stable and in strong trend. EXW price in Shangdong is CNY1,840-1,880/t. In-factory inventory is 507.7kt(-44.4kt), port inventory is 153kt(+2kt). The spring fertilization demand is ended, while industrial demand supports urea price. Urea futures price runs on the high stage and provides support for spot prices. Due to the supply guarantee and price stability policy, urea domesitc price is far lower than the intl’ market price. Intl’ urea price is more than doubled to over CNY5,400/t due to Middle East supply contraction and rising natural gas price. While the rigid demand from India pushes up urea price under the tight supply situation.

Amsul market price fluctuates at a high level this week, with coking grade prices falling and crystal prices strong. Shandong coking grade factory price is CNY1,450-1,525/t (down CNY50-130/t WoW). Caprolactam grade is strongly supported by raw materials cost, offering at above CNY1,800/t. Factories operation rate is low. On demand side: domestic industrial and agricultural demand is stable. Supported by the intl’ urea prices, procurement sentiment for Amsul is bullish in Southeast Asia and South America market, above 80% of China’s Amsul is for export.SCFI is 1,886 (-5), CCFI is 1,211(+1).

USD:CNY is depreciated to 1:6.81 level.