Phosphorus: P4 market had a strong surge in the past two weeks. The average EXW price rose from CNY26,800/t in late March to now CNY30,129/t (above 12% increase in half a month). From supply side, most plants in Yun’nan suspended for facilites maintenance, tightening supply. While traders were reluctant to sell at low prices, leaving limited spot availability. The high cost of phosphate ore, electricity and sulfur provided firm support. From demand side, downstream users (phosphoric acid and glyphosate factories, etc.) actively restocked with strong bullish sentiment. The market is expected to stay high and volatile in the short term, underpinned by tight supply-demand balance.

Sulfur: the market maintained the historical surge, hitting a new high level. Sulfur port price jumped from CNY5,850/t to CNY6,733/t, rose above 15% in two weeks (+500 weekly). Supply side, geopolitical tensions in the Middle East cut shipments arrival by 50%, while the domestic refineries conducted spring overhauls, the supply is pretty tight. Port inventory meets a bottom level in recent years, spot availability is limited and traders are reluctant to sell. Demand side, spring plowing demand for phosphorus fertilizers remained robust. Meanwhile the LFP demand also rises to drive restocking. The market will stay firm and high in the short term.

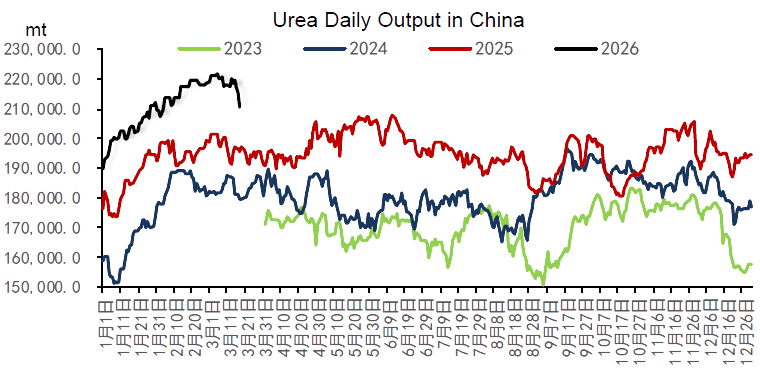

Urea: market stabilized with mild weakness. Futures fell from CNY1,877/t to CNY1,825/t. Spot price ranged CNY1,790~1,840/t. The domestic cap price is strictly controlled within CNY1,850/t. Weekly output is 1,547kt, with an operation rate of 92%. In-factory inventory is 552.1kt(+16.1kt), port inventory is 151kt(-8kt). Spring demand faded while industrial demand still provided support. Low inventories and coal costs limited downside. Compound fertilizer operation rate is 49.6%(-2.9%), Melamine operation rate is 64%. Intl’ market, Middle East tensions tightened supply, driving FOB price up to USD750~820/t.

Amsul Amsul market rose first then stabilized in the past 2 weeks. Caprolactam-grade jumped from CNY1,717/t to CNY1,820/t (+6%), coking-grade price is CNY1,550–1,620/t. Spring farming demand still provides support, while low in-factory inventory kept producers bullish on pricing. Later the high prices constrained purchases, some auctions failed and prices turned downtrend.

Potash: 60% domestic KCl price is CNY2,800~2,950/t, 62% Belarus KCl port price is CNY3,150~3,275/t, down about 30~80/t from early April. Spring farming is ending, the state reserves released above 2.1 million tons, market supply is sufficient.

SCFI is 1,891 (+36), CCFI is 1,210(+2.1%).

USD:CNY is depreciated to 1:6.82 level.