Phosphorus: the market rebounds sharply in the week, showing a strong V-shaped reversal. The benchmark price surges to CNY26,796/t (+6.8% WoW). Supply side, production bases in southwest China face tight supply due to dry season and environmental protection controls. The overall operation rate is 56.75%, slightly up in Yun’nan while stable in Guizhou & Sichuan. Producers jointly hold their offers and limited the sales, traders are also reluctant to sell. Demand side, downstream glyphosate and phosphorus trichloride plants ramp up operations. Spring fertilizers preparation and traders’ restocking drive robust purchases. Trading is active, with high-price deals going smoothly amid strong bullish sentiment.

Sulfur: surged sharply and hit the record high with a one-way bull run. The benchmark jumps from CNY4,967/t to CNY5,920/t (+18% WoW). Yangtze River port granular sulfur exceeds CNY5,900/t, with top deals hitting CNY6,000/t. Tradings are pretty active at high prices amid extreme bullish sentiment. Supply side, over 65% sulfur supply in China depends on import, and 56% of it comes from the Middle East. Port arrivals of imported sulfur in March plummetes about 50% YoY due to shipping disruptions. While the domestic refineries entered spring maintenance, port inventory is down to 1,550kt (5 year bottom level), and traders are reluctant to sell.

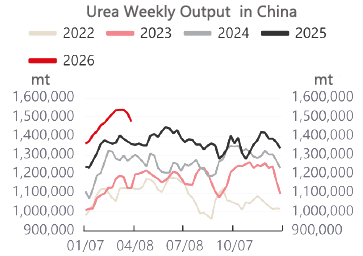

Urea: urea market is weak and price trends lower pressured by ample supply and export policy controls. EXW price is CNY1,800~1,850/t (-3%~5% WoW). On the supply side, the general operation rate stays at a historical high of around 92%, with daily output around 216kt. State reserves (4~5 mln tons) are fully released and flooding the market. On the demand side, spring fertilizers for wheat in northern China area is almost ending. Fertilizer preparation is slow in northeast China. Industrial buyers remains cautious, with only small qty rigid purchases. Since mid March, more and more fertilizers products are restricted to export. Since Tuesday, including calcium nitrate, ammonium chloride are also banned. It seems the restriction would last until Aug. at least.

Amsul the market surges strongly and the price hits a new yearly high (almost approaching urea cost). Caprolactam plants operates at 77% and coking plants at 74%, keeping a low output. While the main producers in south area has facilities maintenance plan, and the high sulfur cost makes market supply further tight. Currently Amsul is the only item can be exported without CIQ inspection, export orders boomed since the international urea price flying high. The benchmark price jumps to CNY1,700/t (+8.3% WoW).

Potash: KCl price is down to CNY3,100~3,300/t, pressured by state reserve releases. SOP is stable at CNY3,850~4,000/t.

SCFI is 1,827 (+120), CCFI is 1,139(+1.6%).