Phosphorus: P4 market is in weak consolidation after previous surge, with benchmark price down to around CNY25,096/t(-1,600/t WoW). The sharp rise in previous 2 weeks triggered the downstream resistance to high cost raw materials, rigid purchases slow down under high price pressure. And some facilities in Yun’nan resumed production, tight supply situation is eased. While the operation rate of glyphosate, phosphoric acid and other downstream sectors is low, P4 demand is not strong. However, raw materials cost support remains, producers hold offers to cap declines. The downstream market sticks to wait & see sentiment.

Sulfur: the market keep on surging strongly, with mainstream port price rise above CNY600/t, breaking through CNY5,300/t. The geopolitical tension in the Middle East cut import volumes, and previoused ordered shipments are also delayed arrivals, pushing port inventories to new low level. The domestic refineries’ maintenance in spring also tighten market supply. From demand side, robust rigid demand for phosphate fertilizers pull up the factories’ operation rate. Traders are also complement their inventory actively. Strong bullish sentiment and hoarding by holders amplified gains. Prices will stay high in the short term.

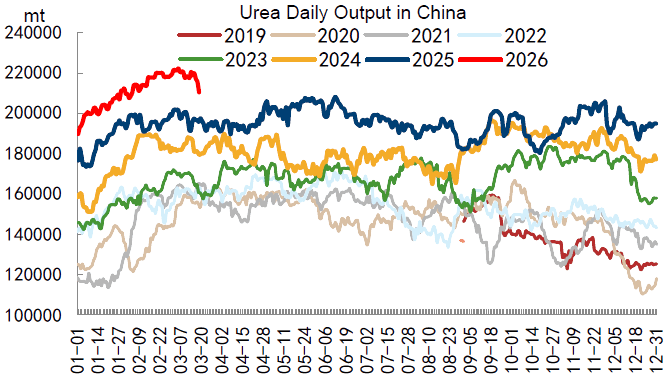

Urea: price is weakened for both spot and futures. Urea EXW price is CNY30–50/t lower WoW, CNY1,820-1,840/t in Shangdong, CNY1,720-1,760/t in Shanxi, and CNY1,800–1,820/t in Henan. The weekly output is 1,519.4kt(-18.2kt), with an operation rate of 92.19%(-1.1%). In-factory inventory is 808.9kt(-148.7kt), port inventory is 167kt(-22kt). Spring fertilization peak season is ending in northern China, agricultural demand is plunged. While market supply is still ample. Besides, state fertilizer reserves are released, flooding the market with low-cost spot products. Urea industrial demand remains soft. Buyer side sticks to a wait-and-see approach.

Amsul production rate is 74%-77%. Coking-grade prices is CNY1,400-1,480/t. Caprolactam-grade in Shandong is CNY1,560-1,580/t. The port inventory remains low and market supply is tight, most producers hold back sales with sufficient backlogs for previous orders. High international urea prices motivate export plans and promptly consume the domestic inventory. Price would remain uptrend.

Potash: Port 62% Belarus KCl is CNY3,530-3,600/t(-30/t). Domestic 60% KCl stands at CNY3,250-3,330/t. SOP 50% powder is CNY3,800-3,900/t. Port inventory is around 272kt, gradually de-stocking, while the domestic production operation rate rebounds and lifting market supply.

SCFI is 1,707 (+218), CCFI is 1,120(+6.2%).