Phosphorus: P4 price fluctuates slightly amid ongoing supply-demand tension. In 1H of the week, price hikes (CNY22,400-22,600/t in Yunnan/Sichuan, >CNY22,600/t in Guizhou) as producers have no inventory pressure and price is supported. But deals are sliding due to the buyers’ resistance to high cost. Avg. prices dip to CNY22,666/t(-0.42% WoW), with sluggish trading reflecting a stalemate between “supply firmness vs. weak demand.”

Phosphoric acid: P.A. avg. price is CNY6,700/t and the market is in stalemate. Hot processed P.A. price is supported by the high yellow phosphorus cost, but downstream phosphate salts and LFP demand is relatively slow, the P.A. operation rate is down to 41.76%. Wet-process P.A. sustained cost pressure from phosphate ore and the rising sulfur price, the operation rate is 63.92%.

Sulfur: Sulfur prices rise broadly. The port solid sulfur price hits CNY2,530/t(+2.08% WoW), liquid sulfur price surges to CNY2,620/t(+2.8% WoW) in Shangdong. Factories’ production becomes tight as the weekly output dip to 231.3kt(-0.17%) amid refinery maintenance, while port inventory rises to 2.5mln tons(+1.68%). Sulfur demand is boosted by the starting autumn fertilizer reserves season, yet the high price results downstream resistance.

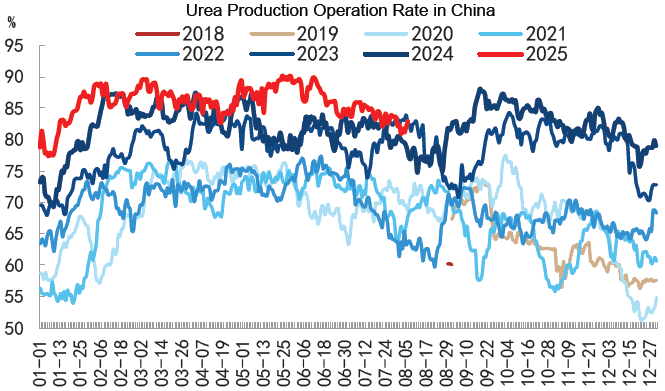

Urea: the market keeps downtrend, with offering below CNY1,700/t (low end urea ~CNY1,650/t) in the mains production bases(Shandong & Henan), while price in Xinjiang plunged to CNY1,400-1,450/t. Supply remains ample with daily output at ~190-200kt and in-factory inventory surges to 957.4kt(+7.86% WoW). Weak agricultural demand and cautious industrial procurement led to a price inversion between factory offers and dealt prices, suppressing the market deals. Amsul price slid to CNY1,113/t(-1.2% WoW) due to oversupply under the sluggish market. Increased operation rate in caprolactam plants boosted the output, while sluggish exports and cautious domestic procurement dampened market trading.

Potash: KCl price held firm, Belarus 62% grade port price is CNY3,150-3,550/t. Qinghai Salt Lake potash supply is tight due to facilities maintenance. Port inventory is about 1.8mln tons, border trade supply remains scarce. SOP Manheim plants operation rate is 40%-45% as raw materials cost is too high. 52% grade powder price is CNY3,900-3,950/t EXW. The operation rate in Xinjing is low to 17.71%, 50% powder delivery price is CNY3,550-3,600/t. Demand remains sluggish.

MAP/DAP: MAP price is stable (Hubei 55% powder: CNY3,425/t), supported by backlog orders.

SCFI is 1,460(-29), CCFI is 1,193(-0.6%).

USD:CNY is relatively stable this week, fluctuates at 1:7.18 level. The probability of Fed cutting interest rates by 25 basis points in September is above 80%.