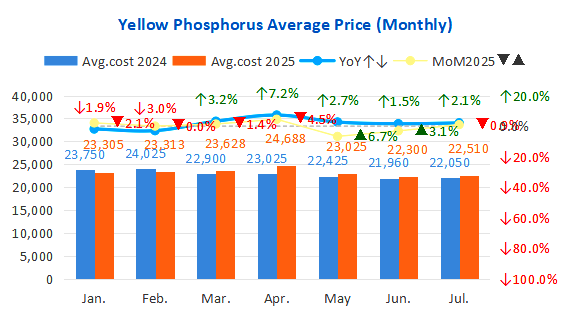

Phosphorus: The yellow phosphorus market has a downtrend performance in July as the downstream demand is sluggish while supply is sufficient. The avg. weekly output rose to 20,510t (operating rate 68.37%), pressing prices lower. By month-end, P4 prices fell to CNY22,300-22,400/t in Yunnan & Sichuan. Demand would remain subdued in Aug. ①Hydro-power cost is still low in the southwest area as rainy season has just started. ②Downstream productions (such as glyphosate) are halted for facilities maintenance. ③Seasonal demand weakness persists. Prices are expected to fluctuate narrowly with limited upside amid weak consumption.

Phosphoric acid: Phosphoric acid prices rose initially (supported by rising yellow phosphorus cost) then fell (driven by sluggish demand) in July, avg. cost remains at CNY6,690/t MoM. It will keep fluctuating in Aug.

Sulfur: Sulfur prices fluctuated on the higher stage, with port inventory surging to 2.57mln tons (+9.20% MoM). In July 1H, declines were driven by weak global prices (Middle East CFR down to USD260-270/t) and dump price from Iran. Demand rebounded and price turned to uptrend in 2H. Yangtze River port prices ranged CNY2,280-2,395/t, avg. price is 0.33% lower marginally. Supply pressure may ease as vessel arrivals decrease, port inventory would decline. Price would be supported by peak fertilizer season (MAP/DAP operating rate>60%) from demand side. However, cautious restocking and slumping phosphate exports (export decreases>60% YoY) would limit the upside.

Urea: Urea prices had an A shape trend in July, monthly-ending at CNY1,812/t(-0.9% MoM). Gains in 1H were driven by optimistic sentiment in nitrogen fertilizer market, but high inventories (in-factory stocks surged to 917.3kt) and weak futures led to declines in 2H. Offers from Shandong&Henan province dropped to CNY1,720-1,810/t, with daily output about 190kt (operation rate about 82%-83.6%). Supply would remain sufficient in Aug., though output would be influenced by facilities mainteinance. Urea demand would stay slow in fertilizer slack season. Compound fertilizer operation rate is 38.68%(+5.1%), melamine capacity utilization rate is 63.50%(-1.7%). Amsul (capro grade) average price slid to CNY1,075/t in Shangdong.

Potash: prices rose initially and then declined under policy guidance. Major producers cut prices to CNY2,800/t (-100/t MoM) EXW for 60% grade KCl. Tight supply (port inventory<1.9mln tons) limited the downtrend. SOP factories faced losses due to high production cost and slow demand. Supply will remain tight in Aug. due to domestic facilities maintenance and limited import, yet demand recovery is sluggish. Autumn fertilizer reservation runs slowly and compound fertilizer procurement is cautious.

MAP/DAP: MAP prices in July were supported by tight supply (inventory down to 159.5kt) and high costs (sulfur +99% YoY). DAP demand was seasonally weak, The intl’ market would be impacted by US new tariff (10%-25% imposed on MENA source) since Aug.7th.

SCFI is 1,550(-42), CCFI is 1,232(-2.3%).

USD:CNY rise to >1:7.2 as Fed remains interest rate.