Phosphorus: the market surged first then eased in the past two weeks (Mar.2–Mar 13). EXW price was above CNY27,000/t and then slid to CNY26,696/t. Supply stayed tight as operation rate in Yunnan, Guizhou and Sichuan remained low on high hydro-electricity power cost and slow resumption in this dry season. Producers controlled shipments and deliveries to support the market prices. Driven by rigid demand from downstream phosphoric acid and glyphosate sectors, the market seems to be bullish as prices jumped quickly. By last weekend, high prices curbed purchases, downstream turned to wait-and-see sentiment and it led to a mild correction on pricing. Supported by costs and tight supply, the market will likely fluctuate at a high level in the short term.

Sulfur: the market surged continuously to new peak in the past two weeks. Supply tightened due to the geopolitical tension in Middle East. Import arrivals are reduced, port inventory stayed low and suppliers halted offers, market price is supported. Robust demand is boosted in this spring fertilization peak season, with high operation rate in phosphate fertilizers production and sulfuric acid sectors. Besides, demand from new energy industries also led to more purchases. The benchmark price jumped from CNY3,803/t to CNY4,750/t. Imported granular sulfur at ports was quoted at CNY4,650–4,700/t. Bullish sentiment prevails amid multiple positives, the market will remain strong on the high stage shortly.

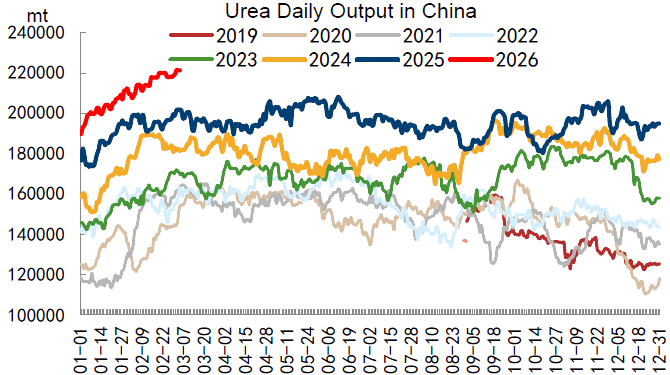

Urea: market steadied first then rose, fluctuating on the high stage. Supply side, operation rate remains 89% with daily output at 210-220kt, indicating ample supply amid state reserves release. Demand was robust during the spring fertilization peak season, driven by wheat topdressing in North China and fertilizer preparation in Northeast China. Downstream purchasing was active, leading to a quick inventory drawdown. Spot prices consolidated mildly earlier then edged up amid stronger futures and rigid demand. Mainstream EXW price in Shandong stood at CNY1,830–1,860/t. The govn’ policy lead-price is put into practice, it makes high prices and speculative restocking curbed. Supported by spring boosting demand but capped by ample supply, the market would remain stable in high range.

Potash: KCl market is stable, while SOP price surged in the past 2 weeks. KCl was capped by price-control policy. Domestic 60% KCl was CNY2,900–3,100/t, port 62% Belarus KCl was CNY3,150–3,600/t, fluctuating in a narrow range. SOP price rallied sharply on high raw materials cost of KCl and sulfuric acid, with Mannheim plants operation rate at only 36%, causing tight supply. 52% powder SOP price rose to CNY4,150–4,300/t. Spring demand lifted compound fertilizer operation rate, especially in Northeast China.

SCFI is 1,489 (+156), CCFI is 1,054(+0.9%).

USD:CNY fluctuates at to 1:6.85-1:6.89 level.