Phosphorus: P4 the market surged after the holidays. P4 supply is tightened due to facilities’ maintenance and slow resumption in Yunnan and Sichuan. While the downstream demand is renewing, it drives P4 price up sharply. EXW price in Yun’nan rose from CNY23,300/t to now above CNY24,000/t, with some even higher offers at CNY24,400/t, marking a weekly increase of nearly CNY900/t. Downstream rigid demand from phosphoric acid and glyphosate picked up, supported by better export expectations. Most producers held prices high and were reluctant to sell at low rates. Supported by cost and tight supply-demand, market sentiment turned bullish with active tradings, and prices would remain high shortly.

Sulfur: market rebounded mildly after stability. Mainstream EXW prices stood at CNY3,790–3,850/t, while port spot prices ranged CNY4,080–4,120/t. Refinery operations were steady with mild inventory pressure. Downstream rigid demand from phosphate fertilizer and sulfuric acid picked up amid spring farming preparation, driving restocking. Producers in Shandong and other regions lifted quotes slightly. Firm Middle East offers and import–domestic price spreads supported the tightening sentiment. Supported by recovering demand and costs, the market is expected to stay firm with potential uptrend in the short term.

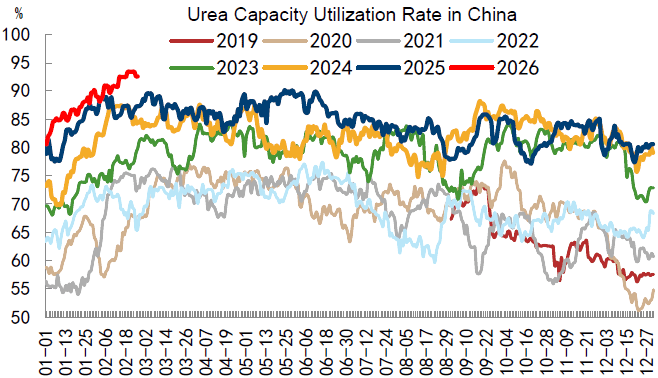

Urea: the benchmark price is CNY1,835/t (+2.3%). Urea weekly output is 1,535.5kt(+1.29%), the operation rate is 93.16%(+1.18%). In-factory inventory rises sharply to 1,176kt(+341.3kt, +40.89%), since trucking was halted during Spring Festival. Port inventory is 174kt(+4.82%). Driven by spring fertilizers restocking coming to peak, urea market is stable with slight gains, price keeps firm on the high stage. Supported by the concentrated demand and rising raw material cost, main production areas saw price increases of CNY10-30/t, with prilled urea prices in Shandong and Henan reaching CNY1,800-1,850/t, EXW. Some actual dealt prices even exceeded official guidance limit. The FOB China price is USD468.5/t(+26/t).

Amsul the market firmly edged up. EXW prices stood at CNY1,180~1,230/t(+2.24% WoW). Supply stayed tight on environmental protection curbs. Downstream compound fertilizer plants restarted and restocked rigidly. Ample export orders and high international urea prices give big support to the market upward sentiment. Producers held prices firmly and were reluctant to sell at low rates. With tight supply-demand and spring fertilization + export support, the market is expected to remain firm with mild potential uptrend in the short term.

Potash: KCl market is high import cost & tight supply, expected to stay strong with limited downsides.

SCFI is 1,333 (+82), CCFI is 1,045(-4%).

USD:CNY is depreciated to 1:6.86 level.