Phosphorus: P4 benchmark price rises marginally to CNY23,846/t(+0.56%). Market offers in Yunnan, Guizhou and Sichuan are between CNY23,350-23,500/t, with actual deals negotiated on a case-by-case basis. On supply side, enterprises maintained stable operation with a daily output of about 2.7kt under the operation rate of 61%, though some electric furnaces in Yunnan and Sichuan are under maintenance, leading to structural contraction of supply. On demand side, pre-holiday stockpiling is almost completed, downstream purchase becomes cautious, only with some rigid demand for hot-processed P.A.

Sulfur: the market first declined then stabilized. Sulfur benchmark price drops to CNY3,983/t (-5.38%). The port price is CNY4,100-4,200/t. On supply side, port inventory falls to a low level of 1.7mln tons, refineries maintain stable operations. From Middle East, FOB contract price of sulfur for February is USD520-530/t (+10/t MoM). The CIF China price is around CNY4,393/t, showing a significant domestic-international price gap. On demand side, pre-holiday stockpiling is ending, downstream phosphate fertilizer and sulfuric acid enterprises purchases are cautious. New order transactions are sluggish, with only little rigid demand replenishment.

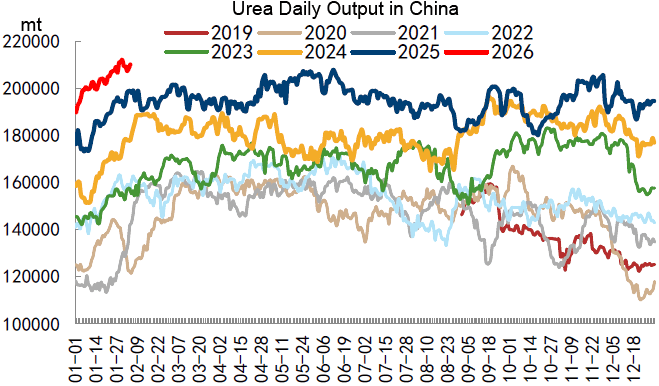

Urea: the benchmark price decreases to CNY1,765/t (-0.98%). The EXW price is CNY1,720-1,770/t in Shandong, Henan, and Shanxi. Urea daily output is nearly 220kt, the operation rate remains stable. The low in-factory inventory supports firm quotations on the market. Demand side, agricultural rigid demand is limited, industrial demand is sluggish, compound fertilizer factories purchasing becomes slow. Stable cost of natural gas and coal provides strong support to urea. The futures market fluctuates within a narrow range, with the main contract UR2605 oscillating between CNY1,770-1,787/t during the week. Traders replenish on rigid demand, end-users are eager to press down prices and stick to wait-and-see sentiment. After a short-term stable and weakening trend, prices may rebound after the Spring Festival holiday with the start of spring plowing demand. The FOB China price is USD422.5/t(+2.5/t).

Amsul price comes up to CNY1,160/t (+0.60%). The caprolactam-grade is CNY1,140-1,160/t and the coking-grade is CNY1,050-1,080/t. Caprolactam plants reduce load by 10%, leading to structural tightening of supply. Stable prices of sulfuric acid and liquid ammonia provided strong cost support.

MAP: powder 55% grade price is CNY3,800-4,400/t, TMAP 73% grade price is CNY6,400-6,600/t. High sulfur and phosphate rock price provides cost support.

SCFI is 1,266 (-50), CCFI is 1,122(-4.5%).

USD:CNY is depreciated to 1:6.93 level.