Phosphorus: the avg. price slid to CNY22,000-22,200/t in Yunnan/Guizhou/Sichuan, down 1.3%-1.35% WoW due to weak demand and increased supply. The operation rate is still high in Yunnan (63.6%) and Guizhou (54.7%). Downstream buyers pressed for lower prices amid cautious sentiment, as demand is not strong. Besides, hydropower-driven electricity price cuts in Southwest China reduced the production cost (e.g., in Sichuan: CNY 0.1/kWh cut results CNY1,500/t cost savings).

Phosphoric acid: the average price of 85% industrial-grade phosphoric acid in China is CNY6,690/t, down 0.30% WoW (monthly decline: 0.59%). H.P. operation rate is 55.95% (down 0.26% WoW), with weekly output at 72,4kt and marginal profit of CNY54/t. Lithium iron phosphate (LFP) price holds steady, with improving energy storage demand expected in July.

Sulfur: the price finally turns to downtrend. Recently the domestic refinery auctions see sharp price cuts, amplifying bearish sentiment. Port inventories surged 12.81% MoM to 2,350.9kt(annual high), driven by the weak purchases and concentrated imports. Fertilizer producers will delay bulk purchases until the inventory pressure eases.

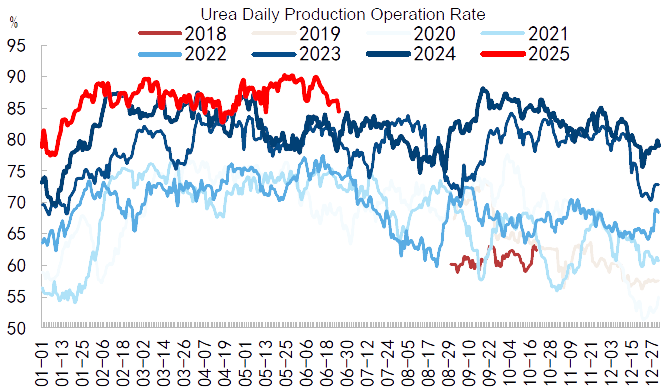

Urea: the dealt price is CNY1,790-1,840/t (+90/t) in Shangdong. the price fluctuates, initially slid (-20-40/t) in Shandong&HeNan due to high output (~200kt/day) and cautious agricultural demand amid weak industrial uptake. Mid-week saw a rebound (+10-30/t) on India’s tender news. However, prices dropped again by weekend(-10-30/t) as oversupply dominated. High inventory and sluggish industrial demand sustain bearish sentiment, with short-term trends remaining volatile and soft. Driven by tightened global urea supply from geopolitical conflicts, Amsul price surges (+26% WoW) at first, the caprolactam grade hits CNY1,300-1,450/t in Shandong. However, easing tension cools the market, and cautious downstream demand lead to declines. By weekend, prices drops to CNY1,150-1,230/t, left +21% rise WoW.

Potash: price rose notably. Imported 62% KCl climbed to CNY3,250-3,400/t as regional conflict disrupting global supply. SOP follows, 52% powder rose to CNY3,700-3,850/t. However, weak demand persists, port inventory remains high (~1.97mln tons), market sticks to cautious sentiment.

MAP/DAP: DAP prices held steady in China, yet global supply is tight. China’s export restriction and Moroccan limited supply pushed India’s import price to $810/t, with stocks down 42% YoY to 124kt.

SCFI is 1,861(-8), CCFI is 1,369 (+2%). Freight to U.S. plunged due to oversupply and postponed shipments. Freight to EU surged 10.62% to $2,030/TEU on carriers’ capacity cuts and planned hikes.